Ancient Economies Reveal Economic Growth Is Unsustainable — Here’s Why

Economic growth facilitated spectacular growth in ancient economies but it also led to their demise. These are the lessons we can apply to our modern context.

Growth is the engine that fuels economic progress. Without it, an economy will stall and eventually collapse.

The more an economy grows, the more you as an individual stand to prosper. At least, in theory. While prosperity is a promise of economic growth, it is far from a guarantee.

The unequal distribution of economic progress has become an issue of political and social contention in recent years. Occupy Wall Street, the rise of Tea Party populism in the United States, and Donald Trump’s election in 2016 reveal a desire for a change in the balance of power.

Throughout history there have been scores of instances of unequal distribution of economic growth. This isn’t purely an American problem. Just as we see happening today, in ancient times growth accumulated with those who had socioeconomic and political power at the expense of those who did not.

While growth at all costs has been the accepted paradigm for modern economists, history tells us that growth is a double-edged sword. As civilization moved from being largely agrarian to becoming increasingly dependent on trade, economic growth generated new financial mechanisms that exacerbated trends toward inequality.

As economic growth accrues within a small percentage of the population, fewer resources remain at the bottom. The workers whose labor is essential for continuing the engine of economic growth, have fewer and fewer resources to generate growth from. As a result, growth in ancient economies stalled, creating the conditions for their eventual demise.

Modern economists look at the state of the world today from a capitalist lens, ignoring the lessons that could be learned from the pre-capitalist era of the ancient world. While neither Babylon nor Greece were capitalist societies, they developed complex economies that facilitated unprecedented growth.

By studying ancient economies we can see the perils of excess growth and develop new ways to foster sustainable economic growth moving forward.

This essay will take lessons from ancient Babylon, Greece, Rome, and the Abbasid Caliphate to illustrate why a growth at all costs economic model is not sustainable. It will specifically highlight the transition from economic growth dominated by agricultural production to economic growth dominated by trade.

It will argue that while trade accelerated new growth opportunities, those opportunities came at a cost that ultimately led to the downfall of these once great civilizations. Without adequate safeguards in place to manage growth, the costs of it can become unsustainable, leading to inequality and inevitable demise.

As we enter into an era of unprecedented economic growth in the current day, the lessons gleaned from the past are more important now than ever before.

Ancient economies centered around agriculture. Surpluses enabled investment in infrastructure projects that led to the rise of skilled craftsmanship and expanded opportunities for commerce.

Wealth is a modern concept if you really think about it. For much of civilization, humans have lived at subsistence. Their goal wasn’t to squirrel away enough money in a 401(k) to eventually retire. It was simply to generate enough caloric energy to survive from one day to the next.

During the Neolithic Revolution, humans began establishing permanent settlements. Agricultural developments made it possible for humans to cultivate crops and store any surpluses that remained.

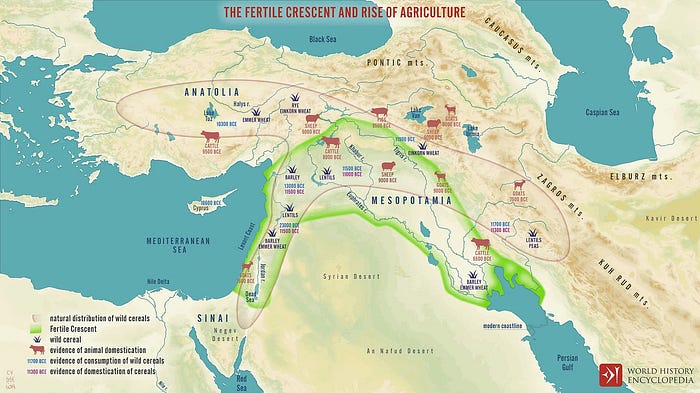

The Middle East is one of the first areas to produce agrarian-based civilizations. Known as the Fertile Crescent, the Middle East provided nutrient-rich soils that supported agricultural cultivation.

One of the first advanced ancient civilizations is that of Babylon. Beginning in the second millennium BCE, Babylon thrived until it was invaded by Persia in the sixth century BCE.

Babylon is an important place to start because it is one of the first empires to provide written records around trade and commerce. These records reveal that trade emerged out of surplus agricultural production. As farmers developed new production methods, they produced more than they needed, generating a surplus they could trade with.

Trade generated what we would refer to today as capital. That capital provided investment in public projects, and in turn, the specialization of labor. These projects enabled workers to learn new skills that they could practice and teach others in their local communities.

As farming techniques improved output, less time was needed to tend to crops. A combination of free time and large-scale building projects gave rise to a class of skilled craftsmen. These craftsmen were able to leverage their skills to produce wares for trade.

Over time Babylon developed enough infrastructure and marketable products to make it a center of trade in the ancient world.

The same pattern of growth also emerged in Ancient Greece. With poor terrain, Greek city-states were limited in what they could grow. They capitalized on the one thing they could produce well — olive oil — and traded it. In time, Greece invested in building a naval presence and ports, enabling the growth of markets in city-states around the Mediterranean.

The ability of ancient civilizations to produce more than they consumed provided the initial capital needed to invest in infrastructure projects. Those projects facilitated the expansion of commerce, taking ancient civilizations from localized city-states and turning them into burgeoning empires.

With the growth of ancient economies came the opportunity to diversify around skilled labor and craftsmanship. Craft, combined with agricultural output, created the products that made travel valuable in the first place.

As commerce took shape and governments invested in a growing number of infrastructure projects, new financial institutions emerged. These financial institutions accelerated opportunities for economic growth.

Over time civilization grew from localized city-states to large empires. The growth of empire naturally facilitated greater degrees of economic interaction with different people across different continents.

This is especially true in the Mediterranean where soil quality limited agricultural output. In Greece, for example, the primary agricultural outputs were olive oil and breeding livestock. Even though upwards of 80% of the population engaged in agricultural activities, olive oil alone was insufficient to support Greece’s population.

Greece became an early center of trade and commerce as a result. The agora enabled the emergence of skilled craftsmanship and provided a space for philosophical debate. Goods were sold according to the demands of the market, providing one of the earliest examples of the implementation of a free market economy.

The rise in commercial transactions necessitated the creation of new financial instruments. Around 600 BCE the first silver coin was minted in Lydia. Up until then, the primary currency of exchange was grain. The introduction of coins and seigniorage established a currency for commercial trade that gradually fell under the purview of government institutions to regulate.

With growing trade and new financial instruments to support growth, new infrastructure projects were commissioned to connect civilizations with one another. Both Rome and the Abbasid Caliphate, for example, invested heavily in the construction of roads while Greece invested in the maintenance of ports and the expansion of trade outposts.

Although trade expanded across the Mediterranean, the means of production were not equally distributed. Targets of conquest tended to correlate with centers of trade and areas abundant in natural resources, like silver mines.

When rival empires weren’t at war with one another they were collecting tribute from the people they ruled. The ability to control commercial ports and collect taxes along trade routes gave ancient civilizations the ability to extract wealth at scale. This reinforced the need to continue creating new infrastructure to support growing trade routes.

The more trade spread the more it necessitated new financial instruments to finance these large infrastructure projects. Banking gave merchants — and the government — access to capital that could be repaid later, allowing them to take risks that previously would not have been possible. Meanwhile, exchange houses emerged as an outgrowth of the use of gold and silver coins across large swaths of territory.

In Rome, banking financed new conquests while in the Abbasid Caliphate early forms of government bond sales facilitated public investment in irrigation projects and public services like education. Shariah law prohibited the collection of interest, pushing Jews and Christians into the banking sector.

One thing that appears to be clear is economic growth is incumbent on trade and the monetization of the economy. The introduction of coins enabled the growth of marketplaces that in turn required substantial infrastructure projects to get goods to market in the first place. From there government institutions and large bureaucracies emerged to regulate trade and collect taxes on.

Over time the new institutions that emerged provided the resources to accelerate economic growth. For a time this growth was reinvested in culture and social well-being, leading ancient civilizations like Greece and Rome to experience golden eras.

While commerce and trade led to the growth of empire, it also fostered a growing gap between the rich and the poor. Unsustainable growth generated inequality that was a major factor leading to the decline of ancient civilizations.

The growth of trade enabled periods of Greek, Roman, and Islamic flourishing. It gave space for art, political thought, and scientific discovery to emerge. But as history shows, not everything is meant to last.

One of the unintended consequences of the rise in trade is the growth of powerful classes within society. Merchants and bureaucrats wielded tremendous power over local populations because they controlled the means to access trade. This enabled select classes of people to monopolize the means of production and methods of trade, allowing them to accrue vast sums of wealth at the expense of the larger population.

Regardless of whether you lived in Rome or Greece, the vast majority of people during this time worked in agriculture and were living at — or slightly above — subsistence levels. They weren’t landowners which meant they didn’t directly benefit from any surpluses they produced. They depended on trading their time for grain and eventually a coin-denominated wage that they could in turn spend on the basic essentials needed to support themselves.

The creation of financial instruments — especially coinage — inevitably led to inflation. Ancient empires increased the flow of money in the economy by mining more silver or conquering gold mines in enemy territory. Moneylenders charged interest on early loans, further contributing to the growing money supply.

This was especially true in Greece where technological advancements made it possible to increase output from silver mining. As the agora grew it demanded more coins to facilitate commercial transactions. The introduction of new coins and the creation of new money from interest-generating banking transactions decreased the purchasing power of the average citizen’s wage, making it difficult to afford the basic necessities.

Over time inequality squeezed the poor and middle class. They took on increasing amounts of debt or moved to larger cities looking for better work opportunities. In time the cost of living reached a point where it was no longer sustainable and the economy ceased to function. Trade slowed and the administrative state grew ineffective.

The breakdown of ancient civilizations wasn’t climactic like revolutionary France, rather it happened gradually over a long period of time. As wealth and power became concentrated at the top it led to the degradation of public services and corruption within the administrative state. Eventually the economy could no longer support continued growth or the existing population, sputtering it to a grinding halt.

Look no further than the fall of Rome to illustrate this point. Rome relied on conquest to generate revenue for its large empire which meant it needed to employ a large army to fight its wars. As the spoils from conquest declined and the costs of maintaining a growing empire rose, Rome lost its ability to provide for its own collective defense. When Germanic tribes invaded in the fifth century CE, there was little Rome could do to stop them.

While economic growth led to the expansion of trade and the creation of massive infrastructure projects that advanced civilization, it also facilitated its decline. The concentration of wealth at the top reduced the productive power of the economic engine of ancient civilizations, making their decline almost inevitable.

Final takeaway.

The ability to generate economic growth through varying means of production enabled ancient economies to thrive. Once they generated a surplus above subsistence, ancient civilizations could invest in infrastructure projects that facilitated trade. Over time, trade led to the growth of institutions that enabled those civilizations to flourish.

What history reveals is that at some point growth becomes unsustainable. Whether it’s power or wealth, when the byproducts of growth accrue at the top, it generates an insatiable appetite for continued growth. Eventually you reach a natural limit where there is nothing left to extract from a population, bringing growth to halt.

Our current economic period isn’t all that dissimilar from ancient times. With 50% of economic participants holding less than 2.5% of America’s wealth, it reveals an unsustainable asymmetry to growth.

Interestingly it was ancient Babylon that came up with a novel solution to solving the economic distribution problem. Hammurabi proclaimed periodic debt jubilees to forgive debts, giving everyone an opportunity to start anew.

Debt jubilees aren’t unique to Babylon. They’re written about in the Old Testament and there are records of debt cancellations in Ancient Egypt. The existence of debt jubilees across different civilizations reveals excess accumulation was a natural byproduct of growth. It’s a consequence that must be mitigated to make continued economic growth sustainable.

In modern times the idea of a debt jubilee is politically unpalatable. Debt is considered a personal obligation, the result of moral indiscretions regarding the use of money. But as ancient civilizations reveal, debt is also the byproduct of unsustainable growth. It is the solution landless workers resort to when they have no other options.

Economists agree there is no such thing as a free lunch; growth is no exception. Economic growth comes at a cost and if that cost is mortgaged against future generations in the form of debt it will eventually lead to economic stagnation and decline.

History reveals what rises can surely fall down. As new technological developments transform the economy and how growth is generated, we would be wise to observe this lesson in the modern day.

This essay is part of a ChatGPT-generated course The History of Modern Economic Thought. Read more about it here.

Tomorrow Today is a member of Amazon’s affiliate program. If you click on a link, Tomorrow Today may be compensated. Thanks for your support.

In response to Tucker's comments, I wholeheartedly agree. The content I've read on this site is impressive, with a well-structured and eloquent presentation. Given the quality, I'm considering subscribing for the $35 annual fee. Although I've subscribed to several Substacks, I believe this one is worth the investment.

In a different post, I appreciated the detailed, organized steps you shared about creating a pre-Substack personal finance site. Although it may not have been as successful as you hoped, I believe that experience will benefit your creative and business endeavors here on Substack. I wish you the best and look forward to your future work.

This is a great topic to write about. Im surprised it has no comments or likes, but I love the effort youre putting in. Keep it up!

In the early American days, there was broadbased land ownership, with varying crops based on the region, and a stable currency. You could float your corn down the mississippi river and it would be sailed to Baltimore to feed the people inventing manufactured goods, etc etc. And the money earned could be saved (gold backed or literal silver/gold), as there were more Americans over time, your money naturally had more purchasing power. Capital expenditures were profitable; not only canals and railroads but also dams for energy and mines- a land of untapped resources. There was a wodmerful symbiosis between every part of the American economy: agriculture/resource extraction, manufacturing, finance.

But over time the land got monopolized, the money got cheap, the manufacturing got outsourced, and the power got centralized- and an understanding of what wealth generation actually is was lost in a fog of consumerism. Sad story, due for a fall, and hopefully a reset.

Keep up the wonderful writing! I’ll read more articles by you